In the long and often opaque history of financial crime in India, few subjects have been as persistently misunderstood, casually misused and blurred as the categorisation of illicit wealth. The popular vocabulary of black money, red money and pink money, though not codified in statutory law, has acquired a certain operational significance. These terms have evolved into practical descriptors that assist to distinguish between tax evasion, criminal acts and aprticular categories of unlawful wealth like narcotics driven income. From a person experience, the failure to clearly distinguish between these categories has real consequences in investigation, prosecutorial success, and ultimately the credibility of the legal system itself.

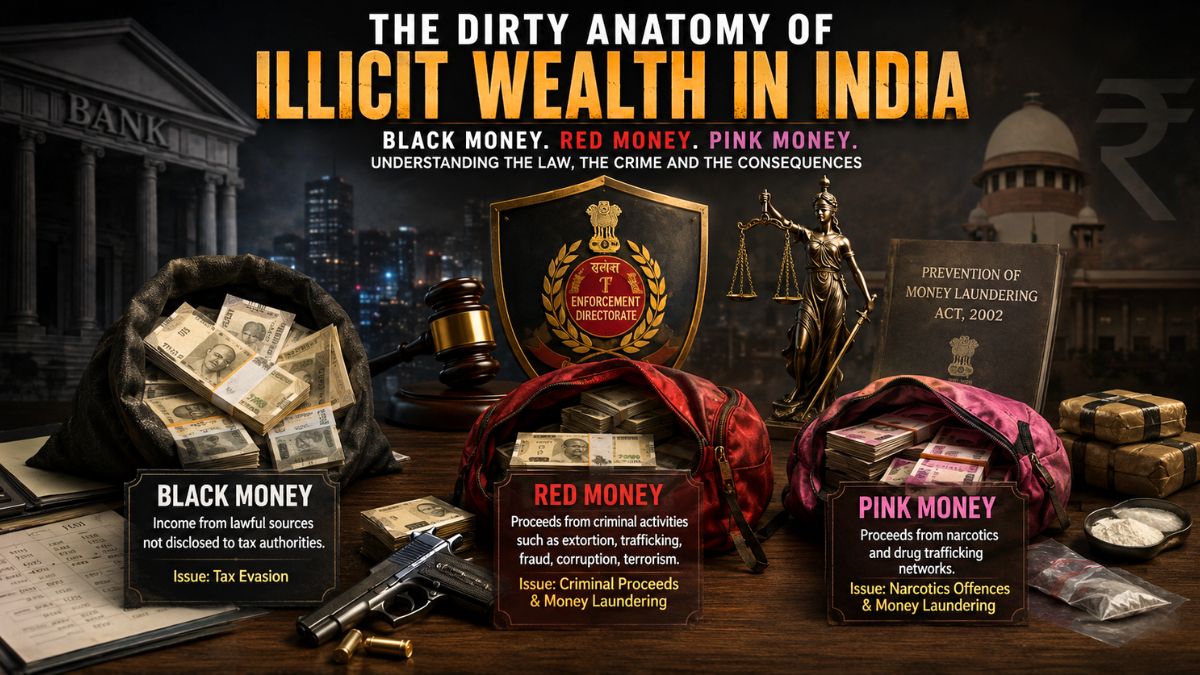

Black money, the most widely recognised of these expressions, is often simplistically equated with illegality in its entirety. That is a dangerous oversimplification. In its truest sense, black money refers to income or assets that have not been disclosed to tax authorities and upon which due taxes have not been paid. The source of such income is not necessarily unlawful. In fact, in a number of cases that I have personally handled or observed, the underlying activity generating the income has been entirely legitimate. Businesses have been underreporting revenue or professionals suppressing fee receipts or even real estate transactions are structured in part cash to minimise stamp duty and tax liability but you see, the illegality arises from the deliberate concealment. This distinction is critical because Indian law treats tax evasion and money laundering as separate, though occasionally overlapping, domains. Proceedings relating to black money are primarily governed by taxation statutes and administered by income tax authorities. The consequences are severe but structurally different from criminal prosecution under anti money laundering laws. These include reassessment of income, imposition of penalties, prosecution for wilful concealment and also attachment of undisclosed assets. However, in the absence of a predicate offence, such concealed income does not automatically qualify as proceeds of crime.

It is here that the legal architecture under the Prevention of Money Laundering Act, 2002 becomes decisive. The statute hinges on the concept of proceeds of crime, which requires that the property in question be derived from a scheduled offence. In my experience, one of the most frequent errors made by investigative authorities in the early years of the Act was the tendency to conflate tax evasion with money laundering. Courts have repeatedly clarified that unless the income is linked to a scheduled offence, mere non-disclosure does not trigger the provisions of the PMLA. This judicial correction has been essential in maintaining the doctrinal integrity of the law.

In contrast, what is colloquially referred to as red money occupies a far more serious and structurally dangerous category. Red money denotes funds generated directly from criminal activities. Unlike black money, where the genesis may be lawful, red money is tainted at its origin. It emerges from offences such as extortion, trafficking, organised crime, kidnapping, terror financing etc. In such cases, the money is not merely concealed but is the product of criminal enterprise itself.

From a prosecutorial aspect to observe, red money cases are fundamentally different in both complexity and urgency. Enforcement agencies are not merely tracing financial irregularities but are dismantling networks that threaten public order and national security. The proceeds are often routed through intricate layers of transactions designed to obscure their origin. I have seen cases where funds generated from organised crime were passed through multiple shell companies, disguised as legitimate business revenue and reintegrated into the formal economy within months. Under the PMLA framework, the handling, possession, concealment, or projection of such funds as untainted constitutes the offence of money laundering. The law empowers authorities to attach properties, conduct searches, seize assets, and prosecute offenders with significant penalties. The evidentiary burden, however, remains complex. Establishing the link between the predicate offence and the financial trail requires a lot with the cross border cooperation.

Pink money, though less frequently discussed in public discourse, represents an equally critical subset of criminal proceeds. It refers informally to funds generated through narcotics and drug trafficking operations. In practical enforcement terms, pink money is treated as a specialised category within the broader framework of criminal proceeds due to its unique operational characteristics and international dimensions.

Drug trafficking networks are among the most sophisticated financial operators in the illicit economy. They rely on layered transactions, benami entities, shell corporations and also some informal transfer systems such as hawala to move funds across jurisdictions. The objective is complete dissociation from the original criminal activity. In one particularly complex matter I recollect, proceeds from narcotics trafficking were routed through three jurisdictions, converted into seemingly legitimate trade payments, and ultimately invested in real estate in India. Tracing such funds required coordination between domestic enforcement agencies and international financial intelligence units.

Offences relating to narcotic drugs fall within the schedule of the PMLA, thereby enabling enforcement agencies to invoke stringent measures. The intersection of narcotics law and anti money laundering legislation creates a powerful enforcement framework, but it also raises concerns regarding due process, evidentiary standards, and the potential for overreach. These concerns are not theoretical. They arise frequently in litigation, particularly in cases involving prolonged attachment of assets and delays in adjudication. The distinction between tax violations and money laundering is defines the scope of state power. Tax evasion, while serious, is fundamentally a fiscal offence. Money laundering, on the other hand, is treated as a threat to economic stability and national security. The investigative mechanisms differ accordingly too. Tax authorities focus on financial disclosure and compliance, whereas enforcement agencies under the PMLA pursue asset tracing, criminal prosecution, and disruption of illicit networks.

In practice, however, the boundaries are not always clear. There are cases where undisclosed income is later found to be linked to criminal activity, thereby transforming black money into proceeds of crime. Conversely, aggressive enforcement has occasionally blurred the line in the opposite direction, treating purely tax related issues as money laundering offences. This tension reflects the broader challenge of balancing effective enforcement with legal safeguards. The role of the banking and financial sector in this ecosystem cannot be overstated. Modern money laundering is rarely a matter of hiding cash in physical form because it is a sophisticated process. Banks, financial institutions and intermediaries are often the channels through which illicit funds are integrated into the legitimate economy.

Regulatory frameworks have evolved to address this challenge. Suspicious transaction reporting, know your customer norms, beneficial ownership identification, and forensic auditing have become central to financial regulation. Yet, despite these measures, laundering techniques continue to evolve. The use of shell companies, fictitious invoicing, and cross border remittances remains prevalent. In several matters I have advised on, the laundering process involved not just domestic entities but a network of offshore jurisdictions designed to exploit regulatory gaps.

Enforcement priorities under the PMLA reflect a clear focus on criminal proceeds rather than mere tax non compliance. Agencies such as the Enforcement Directorate concentrate on cases involving organised crime, narcotics trafficking, corruption, financial fraud, and terror financing. This prioritisation is both pragmatic and necessary, given the scale and impact of such offences.

However, the system is not without its challenges. Delays in investigation, questions regarding the admissibility of evidence, concerns over the reversal of burden of proof, and allegations of selective enforcement continue to shape the discourse around the PMLA. From a policy perspective, there is an ongoing need to refine the balance between enforcement efficiency and procedural fairness. The terminology of black money, red money, and pink money may not find place in statutory texts, but it serves as a useful analytical framework. Black money highlights the issue of tax evasion and financial opacity. Red money underscores the gravity of criminal proceeds linked to organised offences. Pink money draws attention to the specialised and highly structured world of narcotics driven finance.

Understanding these distinctions is not merely an academic exercise. It is essential for legal practitioners, policymakers, and enforcement agencies alike. The classification of funds determines the applicable legal framework, the investigative approach, and the ultimate outcome of proceedings. In a system as complex and evolving as India’s financial regulatory landscape, clarity is not a luxury. It is a necessity.